How to Get Pre-Approved for a Mortgage in 2026: Complete Checklist

Last updated: March 30, 2026

Getting pre-approved for a mortgage typically takes 1-3 business days. You'll need proof of income (W-2s, pay stubs), 2-3 months of bank statements, government-issued ID, and you'll authorize a credit check. In return, a lender gives you a conditional commitment for a specific loan amount — not just a rough estimate, but a real number backed by verified financials.

This is different from pre-qualification, which is based on self-reported information and carries little weight with sellers. Mortgage pre-approval tells you exactly how much house you can afford, makes your offers stronger in competitive markets, and speeds up the closing process once you find the right home.

Here's exactly how to get pre-approved, what documents you need, and how to set yourself up for the strongest application possible.

Pre-Approval vs Pre-Qualification: What's the Difference?

These terms sound interchangeable, but they mean very different things. Pre-qualification is a quick estimate based on what you tell a lender about your income and debts. Pre-approval involves actual verification — the lender pulls your credit, reviews your documents, and issues a conditional commitment.

Here's how they compare:

| Pre-Qualification | Pre-Approval | |

|---|---|---|

| Credit Check | Soft pull or none | Hard pull |

| Documentation | Self-reported | Verified by lender |

| Reliability | Estimate only | Conditional commitment |

| Seller Confidence | Low | High |

| Timeline | Minutes | 1-3 business days |

| Cost | Free | Usually free |

Bottom line: If you're serious about buying, skip pre-qualification and go straight to pre-approval. It's what sellers want to see, and it's the only way to know your real budget. According to the Consumer Financial Protection Bureau (CFPB), getting pre-approved is one of the most important steps in the home buying process.

Documents You'll Need for Mortgage Pre-Approval

The biggest reason pre-approval takes longer than pre-qualification? Document verification. Lenders need to confirm your income, assets, and debts with real paperwork. Gathering everything upfront is the single best way to speed up the process.

Here's your complete mortgage pre-approval document checklist:

Income Verification

- Last 2 years of W-2s — from every employer you've had

- Last 30 days of pay stubs — your most recent, consecutive stubs

- Last 2 years of tax returns — required if you're self-employed, freelance, or have significant non-wage income (1099s, rental income, etc.)

- Profit & loss statement — if self-employed, some lenders want a year-to-date P&L

Asset Verification

- Last 2-3 months of bank statements — all pages, all accounts (checking, savings, investment). Lenders look at these carefully, so don't skip blank pages

- Retirement account statements — 401(k), IRA, or other investment accounts

- Gift letter — if any part of your down payment is a gift from family, you'll need a signed letter stating it's not a loan

Identity & Other Documents

- Government-issued photo ID — driver's license or passport

- Social Security number — for the credit check

- Current mortgage statement — if you already own a home

- Rental payment history — if you're currently renting, some lenders ask for 12 months of proof

- Divorce decree or child support documentation — if applicable, lenders need to understand any legal financial obligations

Pro tip: Create a dedicated folder (digital or physical) for all your mortgage documents before you start. Having everything organized and ready to upload can cut your pre-approval timeline from days to hours.

How to Get Pre-Approved for a Mortgage: Step by Step

Now that you know what you need, here's the process from start to finish. Follow these 7 steps and you'll have your pre-approval letter in hand within a few days.

Step 1: Check Your Credit Score First

Before any lender pulls your credit, know where you stand. You're entitled to free credit reports from all three bureaus (Equifax, Experian, TransUnion) at AnnualCreditReport.com — the only federally authorized source.

Here's what lenders typically require:

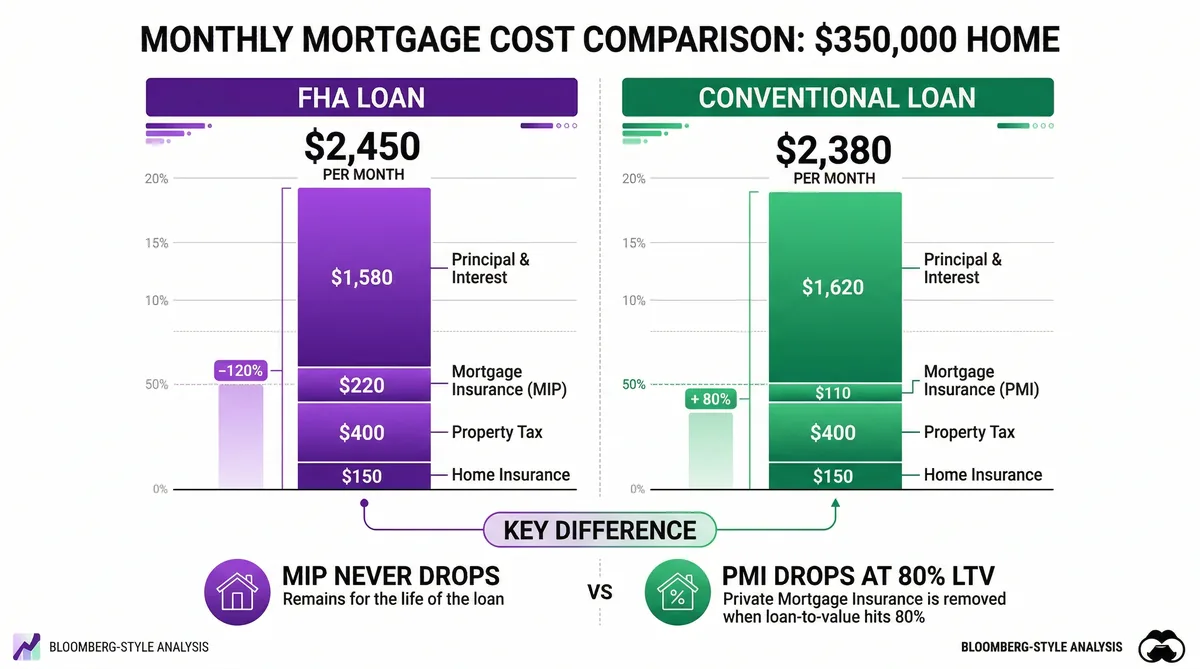

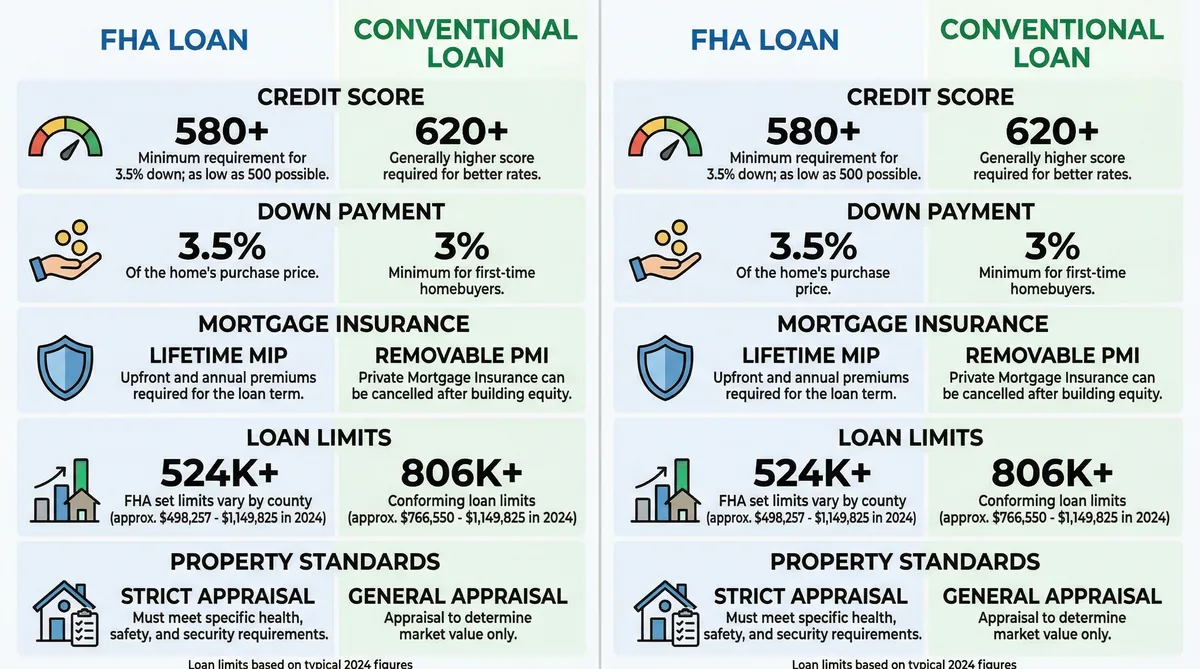

- Conventional loans: 620+ credit score

- FHA loans: 580+ (or 500 with 10% down)

- VA loans: No official minimum, but most lenders want 620+

- USDA loans: 640+ for automatic approval

If your score is below where you need it, don't apply yet. Spend 2-3 months improving it first — the interest rate difference between a 680 and a 740 score can save you tens of thousands over the life of your loan.

Step 2: Calculate Your Budget Using the 28/36 Rule

Before lenders tell you what you can borrow, figure out what you're comfortable paying. The 28/36 rule is the industry standard:

- 28% rule: Your monthly housing payment (mortgage + taxes + insurance) should be no more than 28% of your gross monthly income

- 36% rule: Your total monthly debt payments (housing + car + student loans + credit cards) should stay below 36% of your gross monthly income

Example: If your household earns $8,000/month gross, aim for a housing payment under $2,240 and total debt payments under $2,880.

Step 3: Gather Your Documents

Use the checklist above to collect everything. Most lenders accept digital uploads, so scan or photograph all documents clearly. Make sure bank statements include all pages — even the blank ones that say "This page intentionally left blank." Missing pages are one of the top causes of pre-approval delays.

Step 4: Choose a Lender (Or Get Matched)

You have several options for where to get pre-approved:

- Banks and credit unions — traditional option, sometimes competitive rates for existing customers

- Mortgage brokers — shop multiple lenders on your behalf

- Online lenders — often faster processing, but less personal guidance

- Mortgage matching services — like BEDRWay, which connects you with a dedicated advisor based on your financial profile and loan needs

Shopping around is critical. According to Fannie Mae, borrowers who get quotes from multiple lenders save an average of $1,500 over the life of their loan — and some save much more.

Step 5: Submit Your Application

Once you've chosen a lender, you'll complete a mortgage application (the standardized form is called the Uniform Residential Loan Application, or Form 1003). You'll provide:

- Personal information and employment history

- Income and asset details

- The property type you're looking for

- Your desired loan amount and down payment

This is also when the lender runs a hard credit inquiry. If you're applying with multiple lenders, try to submit all applications within a 14-day window so they count as a single inquiry on your credit report.

Step 6: Wait 1-3 Business Days

After submission, the lender's underwriting team reviews your documents, verifies your information, and makes a decision. Some lenders offer same-day pre-approval for straightforward applications. More complex situations (self-employment, multiple income sources, non-traditional credit) may take up to a week.

During this time, respond immediately to any requests for additional documentation. The faster you provide what they need, the faster you get your letter.

Step 7: Review Your Pre-Approval Letter

Once approved, you'll receive a pre-approval letter that includes:

- The maximum loan amount you're approved for

- The estimated interest rate (may be locked or floating)

- The loan type (conventional, FHA, VA, etc.)

- Any conditions that must be met before final approval

- The expiration date (typically 60-90 days)

Important: Just because you're approved for a certain amount doesn't mean you should borrow that much. Stick to the budget you calculated in Step 2. Lenders approve you for the maximum they think you can repay — but they don't factor in your grocery bill, childcare costs, or retirement savings goals.

How to Strengthen Your Pre-Approval Application

A stronger application doesn't just mean better chances of approval — it means better rates, lower fees, and more negotiating power. Here's how to put your best foot forward.

- Pay down credit card balances. Credit utilization (how much of your available credit you're using) is one of the biggest factors in your credit score. Getting below 30% is good; below 10% is excellent. If you can pay down $2,000 in credit card debt before applying, do it.

- Don't open new credit accounts. Every new credit application creates a hard inquiry and lowers your average account age. Hold off on that new credit card, auto loan, or store financing until after closing.

- Don't change jobs. Lenders want to see stable, consistent employment. Switching jobs — even for higher pay — can complicate your application, especially if it changes your pay structure (salaried to commission, for example).

- Save for a larger down payment. A bigger down payment means a lower loan-to-value (LTV) ratio, which reduces the lender's risk. Put down 20% or more and you'll also avoid private mortgage insurance (PMI), saving you $100-300/month.

- Fix credit report errors before applying. About 1 in 5 consumers has an error on at least one credit report, according to the FTC. Dispute inaccuracies with the credit bureaus before your lender pulls your report.

- Keep large deposits documented. If you receive a large deposit (gift, bonus, sale of an asset), keep a clear paper trail. Unexplained deposits raise red flags with underwriters because they need to verify the money isn't a loan you'll need to repay.

What Can Go Wrong After Pre-Approval

Getting pre-approved is a milestone — but it's not a guarantee. Your pre-approval is conditional, meaning the lender can withdraw it if your financial picture changes. Here are the most common deal-killers between pre-approval and closing.

- Changing jobs or losing income. If your employment status changes, the lender will re-evaluate. Even a lateral move can trigger a delay because the lender needs to re-verify your income.

- Taking on new debt. That new car loan or furniture financing changes your debt-to-income (DTI) ratio. Lenders check your credit again before closing, and new debt can push you over the limit. The CFPB recommends keeping your DTI below 43% for most loan types.

- Large unexplained deposits. A sudden $10,000 deposit with no documentation? Underwriters will flag it. If you receive large sums between pre-approval and closing, document the source immediately.

- Co-signing for someone else. When you co-sign a loan, that debt counts on your DTI ratio — even if someone else is making the payments. This can disqualify you overnight.

- Property appraisal comes in low. This isn't about you — it's about the house. If the appraised value is lower than the purchase price, the lender won't approve the full loan amount. You'll need to renegotiate the price, make up the difference in cash, or walk away.

Golden rule: From the day you get pre-approved until the day you close, change nothing. Don't open accounts, don't close accounts, don't make large purchases, and don't switch jobs. Keep your finances exactly as they were when you got approved.

How Long Does Pre-Approval Last?

Mortgage pre-approval typically lasts 60-90 days, depending on the lender. After that, you'll need to re-apply with updated documents because your financial situation — and interest rates — may have changed.

Here's what to know about the timeline:

- 60 days is the most common expiration period

- 90 days is offered by some lenders, especially for well-qualified borrowers

- Re-approval is faster than the initial process — the lender already has your file, so they just need updated pay stubs, bank statements, and a fresh credit pull

- Interest rates may change. Your pre-approval rate isn't locked unless you specifically request (and sometimes pay for) a rate lock. Market conditions can shift your rate between pre-approval and your offer being accepted

- Multiple renewals are fine. If your home search takes longer than expected, getting re-approved every 60-90 days won't hurt your chances. Lenders understand that finding the right home takes time

Tip: If your pre-approval is expiring soon and you're close to making an offer, ask your lender for an extension or a quick re-verification. Most will accommodate reasonable requests to avoid losing your business.

Key Takeaways

- Pre-approval takes 1-3 business days and gives you a conditional commitment for a specific loan amount — far stronger than a pre-qualification estimate

- Gather documents early: W-2s, pay stubs, bank statements, tax returns, and photo ID. Having everything ready can cut your timeline significantly

- Check your credit first at AnnualCreditReport.com — know your score and fix errors before any lender pulls your report

- Compare multiple lenders. Getting quotes from 3-5 lenders within a 14-day window counts as a single credit inquiry and can save you thousands

- Don't change your finances after pre-approval. No new debt, no job changes, no large unexplained deposits — keep everything stable until closing

- Pre-approval expires in 60-90 days but re-approval is faster. Don't let expiration stress you — it's a normal part of a longer home search

Ready to Get Pre-Approved?

BEDRWay matches you with a dedicated mortgage advisor who handles the entire pre-approval process. 60 seconds to start. No credit pull until you're ready.

Start My Pre-Approval →Frequently Asked Questions

Yes, mortgage pre-approval requires a hard credit inquiry, which can lower your score by 2-5 points temporarily. However, if you apply with multiple lenders within a 14-45 day window (depending on the scoring model), all inquiries count as a single pull. The minor dip recovers within a few months, and the benefit of knowing your exact approval amount far outweighs the temporary impact.

Yes, you can get pre-approved with lower credit scores, though your options will be more limited. FHA loans accept scores as low as 580 (or 500 with a 10% down payment). VA loans have no minimum score requirement set by the VA, though individual lenders may set their own. Some non-QM lenders work with scores below 580. You may face higher interest rates and need a larger down payment, but pre-approval is still possible.

Aim for 3-5 lenders to compare rates, fees, and terms. As long as you complete all applications within a 14-45 day window, multiple hard credit pulls count as a single inquiry on your credit report. Comparing lenders can save you tens of thousands of dollars over the life of your loan. BEDRWay simplifies this by matching you with the best-fit advisor based on your specific financial profile.

Pre-approval is a conditional commitment based on your financial information before you find a property. Final approval (also called "clear to close") happens after the lender verifies the specific property through an appraisal, completes a title search, and does a final review of your finances. Pre-approval says "you can likely borrow up to $X." Final approval says "you are approved to purchase this specific property at this price."

Yes, pre-approval can be revoked if your financial situation changes. Common reasons include job loss or income reduction, taking on new debt (car loan, credit card, furniture financing), large unexplained bank deposits, credit score drops, or the property appraisal coming in below the purchase price. To protect your pre-approval, avoid making any major financial changes between pre-approval and closing.

Absolutely. Getting pre-approved before house hunting gives you three major advantages: you know your exact budget so you only look at homes you can afford, sellers take your offers more seriously (especially in competitive markets), and you can close faster because the financial vetting is already done. Most real estate agents won't even schedule showings without a pre-approval letter.