First-Time Home Buyer Guide 2026: Steps, Programs & Expert Tips

Last updated: March 30, 2026

Buying your first home comes down to 8 steps: check your credit score, save for a down payment, get pre-approved for a mortgage, find a real estate agent, search for homes within your budget, make an offer, complete the inspection and appraisal, and close. The entire process takes 3 to 6 months from start to finish, and you don't need 20% down — most first-time buyers put down 3% to 5%.

This first-time home buyer guide walks you through every step, explains the loan programs available in 2026, and highlights the mistakes that cost buyers thousands. Whether you're just starting to think about homeownership or you're ready to get pre-approved this week, you'll find specific numbers, timelines, and action items below.

The biggest thing to know upfront: you don't need perfect credit, a huge savings account, or a finance degree. You need a plan. That's what this guide gives you.

How Much Home Can You Actually Afford?

Before you look at a single listing, figure out what you can comfortably afford — not what a lender says you qualify for. These two numbers are often very different.

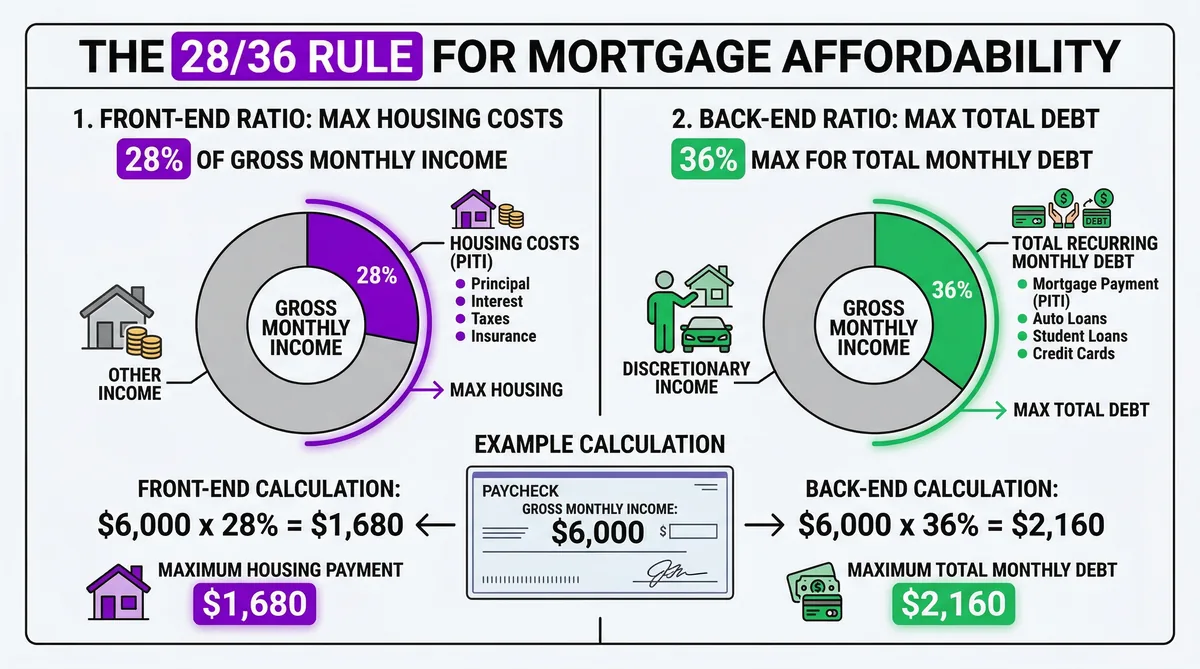

The 28/36 Rule

Most financial experts recommend the 28/36 rule:

- 28% — Your monthly mortgage payment (principal, interest, taxes, insurance) should not exceed 28% of your gross monthly income.

- 36% — Your total monthly debt payments (mortgage + car loans + student loans + credit cards) should stay below 36% of gross income.

Here's what that looks like in practice:

| Household Income | Max Monthly Mortgage (28%) | Approximate Home Price* |

|---|---|---|

| $60,000/yr | $1,400/mo | $230,000 – $260,000 |

| $80,000/yr | $1,867/mo | $310,000 – $350,000 |

| $100,000/yr | $2,333/mo | $390,000 – $440,000 |

| $120,000/yr | $2,800/mo | $470,000 – $530,000 |

| $150,000/yr | $3,500/mo | $590,000 – $660,000 |

*Assumes 6.5% rate, 5% down, includes estimated taxes & insurance. Your actual number depends on your rate, down payment, and location.

Why lender pre-qualification amounts feel too high: Lenders often approve you based on a 43% to 50% DTI ratio — far above the 28/36 comfort zone. A lender might say you qualify for $450,000, but at that level you'd be spending over 40% of your income on housing. Stick to the 28% guideline and you'll still be able to save, travel, and handle emergencies.

Step-by-Step: Buying Your First Home in 2026

Here's your first-time home buyer checklist — the steps to buying a house in the order you should actually follow them.

Step 1: Check Your Credit Score

Your credit score determines which loan programs you qualify for and what interest rate you'll get. Pull your free credit report at AnnualCreditReport.com and check your FICO score.

Here are the minimums by loan type:

- Conventional loan: 620+ (best rates at 740+)

- FHA loan: 580+ for 3.5% down (500-579 requires 10% down)

- VA loan: No government minimum, but most lenders want 580-620

- USDA loan: Typically 640+

If your score is below 620, spend 2-3 months paying down credit card balances (keep utilization under 30%), correcting errors on your report, and avoiding new credit applications.

Step 2: Save for Your Down Payment

You don't need 20% down. Here's what you actually need:

- 3% down — Conventional loan (Fannie Mae HomeReady, Freddie Mac Home Possible)

- 3.5% down — FHA loan

- 0% down — VA loan (veterans/active military) or USDA loan (eligible rural areas)

On a $350,000 home, 3% down is $10,500. Also budget 2% to 5% of the home price for closing costs ($7,000 – $17,500 on a $350K home). Many states offer down payment assistance grants that can cover part or all of this.

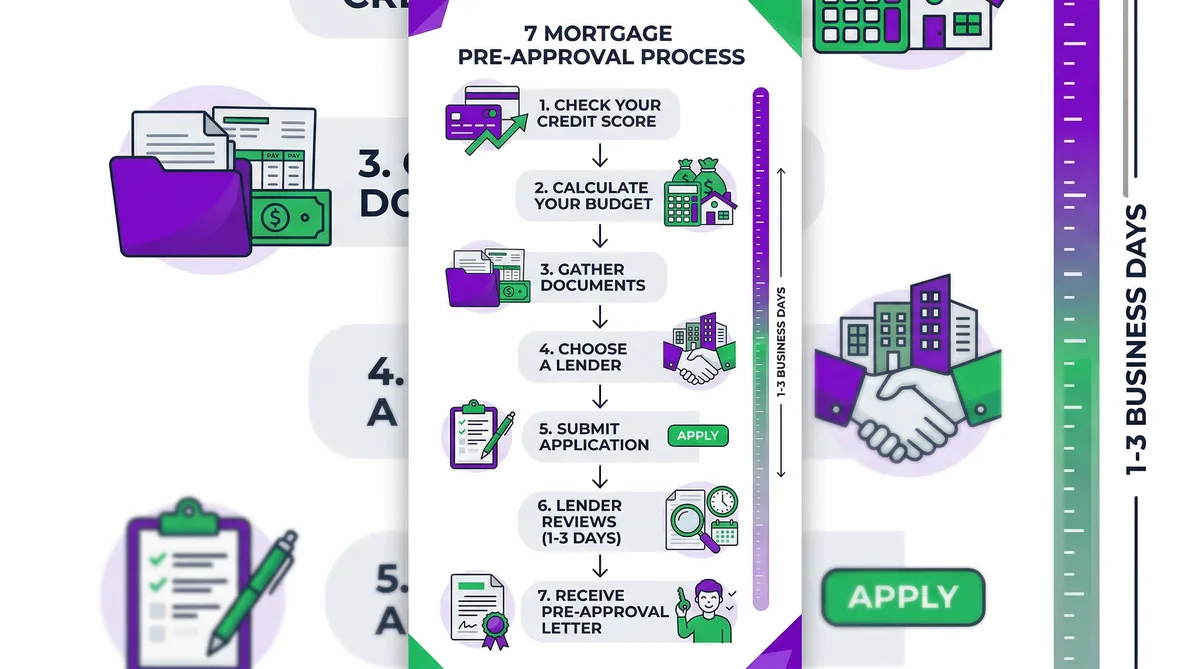

Step 3: Get Pre-Approved

Pre-approval is the single most important step before house hunting. A lender reviews your income, assets, debts, and credit — then gives you a letter stating exactly how much they'll lend you.

You'll need: pay stubs (30 days), W-2s/tax returns (2 years), bank statements (2-3 months), and a valid government ID. The process takes 1-3 business days.

Read our full pre-approval checklist →

Step 4: Find a Real Estate Agent

A buyer's agent represents your interests, helps you find homes, writes offers, and negotiates on your behalf. In most transactions, the seller pays the buyer's agent commission — so this expertise costs you nothing out of pocket.

Look for an agent who specializes in your target area and has experience with first-time buyers. Ask for references and interview at least 2-3 agents before choosing.

Step 5: House Hunt With Your Pre-Approval Letter

Search within your pre-approved amount or below. Make a list of must-haves vs. nice-to-haves before you start. Visit at least 5-10 homes before making an offer — this gives you a feel for what different price points look like in your market.

Pay attention to: location and commute, school districts (even if you don't have kids — they affect resale value), property taxes, HOA fees, and the overall condition of the home.

Step 6: Make an Offer

Your agent will help you write a competitive offer based on comparable sales in the area. Key components include: offer price, earnest money deposit (typically 1-3% of the price), contingencies (inspection, appraisal, financing), and your desired closing date.

In competitive markets, sellers may receive multiple offers. Your pre-approval letter makes your offer stronger than buyers who only have a pre-qualification.

Step 7: Home Inspection & Appraisal

The home inspection ($300 – $500) checks for structural issues, roof damage, plumbing problems, electrical defects, and more. Never skip this. If major issues are found, you can negotiate repairs, request a price reduction, or walk away.

The appraisal ($400 – $600) is ordered by your lender to confirm the home is worth what you're paying. If the appraisal comes in lower than your offer price, you'll need to negotiate with the seller, make up the difference in cash, or renegotiate the price.

Step 8: Close on Your Home

Closing day typically happens 30-45 days after your offer is accepted. You'll do a final walk-through of the property, sign a stack of documents, pay your down payment and closing costs, and receive the keys.

Closing costs typically range from 2% to 5% of the loan amount and include: origination fees, title insurance, attorney fees, prepaid taxes and insurance, and recording fees. Ask your lender for a Closing Disclosure at least 3 days before closing so there are no surprises.

Ready to See What You Qualify For?

Get matched with a dedicated mortgage advisor. No credit pull. No spam. Real numbers in 60 seconds.

Check My Loan Options →First-Time Home Buyer Programs You Should Know

There are first-time home buyer programs in 2026 at the federal, state, and local level. Here's a quick comparison of the major loan types:

| Program | Min. Down Payment | Min. Credit Score | Mortgage Insurance | Best For |

|---|---|---|---|---|

| Conventional (3% down) | 3% | 620 | PMI until 20% equity | Good credit, want to drop MI later |

| FHA Loan | 3.5% | 580 | MIP for life of loan* | Lower credit scores, smaller down payment |

| VA Loan | 0% | No gov. minimum | None (funding fee instead) | Veterans, active military, surviving spouses |

| USDA Loan | 0% | 640 | Guarantee fee (low) | Rural & suburban buyers, moderate income |

| HomeReady / Home Possible | 3% | 620 | Reduced PMI | Low-to-moderate income buyers |

*FHA MIP can be removed by refinancing into a conventional loan once you have 20% equity.

FHA vs Conventional Loan: full comparison →

State Down Payment Assistance Programs

Nearly every state has a housing finance authority that offers down payment assistance (DPA) to first-time buyers. These programs typically provide $5,000 to $25,000+ as grants, forgivable loans, or low-interest second mortgages.

Eligibility usually depends on your income (often up to 80-120% of area median income), the home price, and whether you've completed a homebuyer education course. Search your state's HFA website or ask your mortgage advisor which programs apply to you.

Down Payment: How Much Do You Really Need?

The 20% down payment is a myth for most first-time buyers. According to the National Association of Realtors, the typical first-time buyer puts down 6% to 8%.

Here's what different down payment levels look like on a $350,000 home:

| Down Payment % | Cash Needed | Loan Amount | Est. Monthly PMI* |

|---|---|---|---|

| 3% | $10,500 | $339,500 | $120 – $170/mo |

| 3.5% (FHA) | $12,250 | $337,750 | MIP ~$145/mo |

| 5% | $17,500 | $332,500 | $100 – $150/mo |

| 10% | $35,000 | $315,000 | $60 – $100/mo |

| 20% | $70,000 | $280,000 | $0 |

*PMI estimates based on 680+ credit score. Actual costs vary by lender and loan program.

PMI isn't permanent. On conventional loans, you can request PMI removal once you reach 20% equity, and it automatically drops off at 22%. For many buyers, paying $100-$150/month in PMI for a few years is far better than waiting years to save up $70,000.

Where Your Down Payment Can Come From

- Personal savings — Checking, savings, money market accounts

- Gift funds — Conventional and FHA loans allow gifts from family members (you'll need a gift letter)

- Down payment assistance — State/local grants and forgivable loans

- 401(k) loans — You can borrow from your retirement account (not recommended, but possible)

- IRA withdrawal — First-time buyers can withdraw up to $10,000 penalty-free from a traditional IRA

Common Mistakes First-Time Buyers Make

These are the errors that cost first-time buyers the most money and stress. Avoid all six.

1. Not Getting Pre-Approved First

House hunting without pre-approval is like grocery shopping without knowing your budget. You'll waste time looking at homes you can't afford and your offers won't be taken seriously. Get pre-approved before you visit a single open house.

2. Skipping the Home Inspection

Saving $400 on an inspection can cost you $10,000 – $50,000+ in hidden repairs. Foundation cracks, mold, faulty wiring, and roof damage aren't visible during a walkthrough. Always get an inspection, even in competitive markets where sellers ask you to waive it.

3. Maxing Out Your Budget

Just because a lender approves you for $400,000 doesn't mean you should spend $400,000. Leave room for unexpected repairs, property tax increases, and life changes. Buy at 80-90% of your max approved amount and you'll sleep much better at night.

4. Ignoring Closing Costs

First-time buyers often budget for the down payment and forget about closing costs, which add 2% to 5% of the loan amount. On a $350,000 home, that's an extra $7,000 to $17,500 due at closing. Ask your lender for an estimate early so you're not scrambling at the end.

5. Not Shopping Multiple Lenders

The Consumer Financial Protection Bureau (CFPB) recommends getting quotes from at least 3-5 lenders. Even a 0.25% difference in interest rate saves you $15,000 to $20,000 over 30 years on a $350,000 loan. All hard credit pulls within a 14-45 day window count as a single inquiry, so there's no penalty for shopping around.

6. Making Big Purchases Before Closing

Do not buy a car, open a new credit card, finance furniture, or change jobs between pre-approval and closing. Lenders check your credit and employment again before funding the loan. Any changes to your debt or income can kill your mortgage approval at the last minute.

Key Takeaways

- You don't need 20% down. Most first-time buyers put down 3% to 5%, and programs like VA and USDA offer 0% down.

- Get pre-approved before house hunting. It sets your budget, strengthens your offers, and saves you time.

- Use the 28/36 rule for affordability. Don't let a lender's max approval push you past your comfort zone.

- Check first-time buyer programs. FHA, VA, USDA, HomeReady, and state DPA programs can save you thousands.

- Budget for closing costs. Plan for 2-5% of the loan amount on top of your down payment.

- Shop at least 3-5 lenders. A small rate difference saves $15,000+ over the life of the loan.

Ready to See What You Qualify For?

Get matched with a dedicated mortgage advisor. No credit pull. No spam. Real numbers in 60 seconds.

Check My Loan Options →